Open enrollment is the period of time in the year when an employee can either re-select or change benefits without needing a qualifying life event. Open enrollment is not held during the same period for every company. Open enrollment is typically open right before the beginning of a new benefit year. The benefit year is a 52-week period that defines when an individual can receive benefits based on their previous employment. During the open enrollment period, you have an important opportunity to make decisions about your healthcare benefits for the upcoming year.

During my 12 years of working in human resources, I’ve noticed that things normally get a bit confusing for employees when we introduce varying plan types, FSA and HSA. Choosing between a Flexible Spending Account (FSA) and a Health Savings Account (HSA) can significantly affect your finances and how you manage medical expenses. Both FSAs and HSAs offer tax advantages, helping you save money on healthcare by using pre-tax dollars to cover eligible expenses.

Understanding the features of each account type can guide you to make the best choice for your situation. Your healthcare needs and financial goals should inform whether an FSA or HSA is better suited for you. Consider how much you might spend on healthcare and whether the flexibility of an HSA aligns with your future plans. This post will completely explain all of the confusing aspects of open enrollment and make choosing benefits a less stressful time for you.

Eligibility and Enrollment

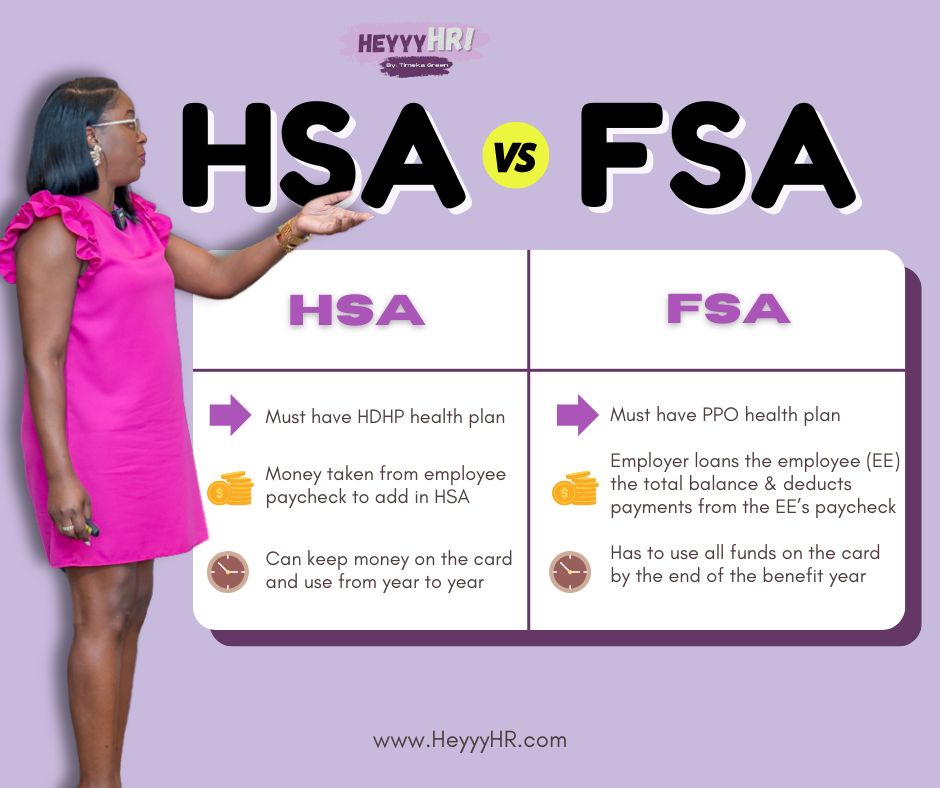

During the open enrollment period, you can make important decisions related to your health plans, such as determining your eligibility for Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Enrolling in HSA and FSA allows you to set aside money for medical costs not covered by your medical/health plan. You can enroll in an FSA during open enrollment or within 30d days of a qualifying life event. An HSA, on the other hand, requires a high-deductible health plan (HDHP) but offers the benefit of funds rolling over annually, unlike FSAs where funds can be forfeited if not used.

To be eligible for a Health Savings Account (HSA), you must be enrolled in a high-deductible health plan (HDHP). This type of plan typically has lower premiums (amount deducted from your paycheck) but requires you to pay more out-of-pocket before insurance covers costs.

Eligibility for an FSA does not always depend on having an HDHP. Any employee whose company offers an FSA can participate. Both accounts allow you to set aside pre-tax money for qualified medical expenses, but they have different rules and limits.

HSA:

- Enrollment in a High-Deductible Health Plan (HDHP)

- Not enrolled in Medicare or any other health coverage conflicting with HSA

- Can keep the money on the card from year to year (no “use or lose” rule)

- Funds are deducted from an employee’s paycheck

- Can change contributions (amount from your paycheck) as often during the year

- Can receive a tax deduction when filing annual taxes

FSA:

- The entire amount of the loan provided by your employer

- Enroll during open enrollment or after qualifying events

- Must use all funds during the benefit year or will lose the balance

Open Enrollment Process for FSA and HSA

Open enrollment is the time when you can sign up for an HSA or FSA but that is completely based on the type of medical plan that you have selected. During this period, you can choose your contributions and confirm your participation for the upcoming benefit year. It’s important to review plan details as limits and policies can change from year to year.

For HSAs, you must decide the contribution amount that will be deducted from your paycheck. You can adjust the amount that is deducted from your paycheck later in the year. FSAs require you to use employer-contributed funds within the plan year or risk losing the unused portion, though some plans may offer a rollover option.

Enrollment Steps:

- Review available medical plans.

- Choose contribution amounts.

- Submit selections during open enrollment (online or via paper/forms).

- Confirm any carryover options for FSAs.

What Are FSA and HSA?

Health savings accounts (HSAs) and flexible spending accounts (FSAs) are special savings plans that help pay for medical expenses using pre-tax dollars. HSAs offer the ability to carry over unused funds year after year, while FSAs are typically “use it or lose it” within the plan year.

Understanding Flexible Spending Accounts (FSA)

Flexible spending accounts (FSAs) are set up through your employer. This is done only three times in the benefit year. Those times are when you’re hired during new hire orientation, within 30 days of a qualifying life event, or during open enrollment.

These accounts let you save money pre-tax for eligible healthcare expenses like doctor visits, prescriptions, and dental care. During open enrollment, you decide how much to contribute up to an annual limit set by the IRS.

Employers will add money to your FSA, and then deduct the money from your paycheck over time. Essentially, your employer has given a loan to you for medical or medically-related needs. The repayment is divided equally from each paycheck throughout the benefit year. Some employers will add additional funds that employees are not required to repay, but this is not common.

An important feature is the spend-it-or-lose-it rule, meaning any unspent funds at the end of the year—except for a possible small carryover or grace period—are forfeited. These accounts provide a way to save on taxes while covering essential medical costs. Using an FSA for planned expenses can benefit those with predictable healthcare spending (i.e. planned surgeries, pregnancies, etc.).

The Basics of Health Savings Accounts (HSA)

Heath savings accounts (HSA) are set up through your employer as well. This is done only three times in the benefit year. Those times are when you’re hired during new hire orientation, within 30 days of a qualifying life event, or during open enrollment.

Health savings accounts (HSAs) are available to people with high-deductible health plans. With an HSA, you contribute pre-tax dollars, saving on income taxes, which can then pay for qualified medical expenses. As with the FSA, there are annual limits set by the IRS.

One major advantage is that you can roll over unused funds year after year, allowing the balance to grow. Contributions can be made through payroll deductions, and, unlike FSAs, you own the HSA and keep it even if you change jobs. HSAs can also serve as a long-term savings tool, as they earn interest and can be invested. This makes HSAs a flexible option for managing healthcare costs over time. In some cases, after separating from an organization, you can roll the remaining funds into your eligible retirement plan.

Managing Your Accounts

Effectively managing your HSA or FSA involves understanding how to handle expenses and utilize available investment options. Knowing how to reimburse yourself for medical or health-related expenses and making strategic investment choices can maximize the benefits of these accounts.

FSA & HSA: Expenses and Reimbursements

When managing your HSA or FSA, it’s essential to keep track of qualified medical expenses. These expenses include doctor visits, prescription medications, and certain medical supplies. Keeping all your receipts and documentation organized helps when it’s time to request a reimbursement or if the third-party company requests receipt(s) or does an audit on your account.

For FSAs, you generally have to use the funds by the end of the year, which requires careful planning. HSAs, however, allow unused funds to roll over, giving you more flexibility. You can use an HSA debit card for direct payments, or pay out-of-pocket and later reimburse yourself from the account.

Using a consistent system to track expenses ensures you meet guidelines and maximize your accounts effectively.

HSA: Investment Options and Strategies

With an HSA, investing options can play a significant role in long-term savings growth. Once your account balance exceeds a certain threshold, many HSA providers allow you to invest in mutual funds and other financial products. Reviewing your investment objectives and understanding risks is crucial before making any decisions.

Choosing investments that align with your risk tolerance and financial goals can enhance the value of your savings. Consider both conservative and growth-oriented strategies based on your future medical expense needs and retirement plans.

Maintaining a well-informed approach to account management facilitates potential growth over time and can provide substantial benefits in managing healthcare costs.

Contribution Limits and Tax Benefits

Understanding the contribution limits and tax benefits of HSAs and FSAs can help you save money on healthcare expenses. The IRS sets these limits annually, and they come with valuable tax advantages.

Annual Contribution Limits for 2024 & 2025

Each year, the IRS updates the contribution limits for Health Savings Accounts (HSA) and Flexible Spending Arrangements (FSA). For 2024, the HSA limit is $4,300 for individuals and $8,550 for families. If you are 55 or older, you can add an extra $1,000 as a catch-up contribution. FSAs for 2024 allow up to $3,200 in contributions. For 2025, this FSA limit will increase to $3,300. Ensure you understand these limits to maximize tax savings and manage healthcare expenses effectively.

Tax Advantages of HSA and FSA

HSAs and FSAs offer significant tax advantages. Contributions to HSAs are tax-deductible, and withdrawals for qualified healthcare expenses are tax-free. Unused HSA balances roll over yearly and can grow tax-free. FSAs provide tax-free funds to pay for eligible medical expenses, but remember that these accounts often have “use-it-or-lose-it” rules, though some allow limited carryover. Consulting a tax advisor or reviewing IRS Publication 502 can provide you with detailed guidelines for these benefits. Using these accounts wisely can lead to substantial savings on your taxes and healthcare costs.

Frequently Asked Questions (FAQs)

Understanding the differences and eligibility requirements for FSAs and HSAs during open enrollment can help you make informed decisions. Knowing whether you can participate in both and the benefits of each can guide your choices.

What are the eligibility requirements to enroll in an FSA during open enrollment?

To enroll in a Flexible Spending Account (FSA), your employer must offer this option. Typically, you must sign up during the open enrollment period unless you qualify for a special enrollment due to a major life event, such as marriage or birth of a child.

How do FSA contributions differ from HSA contributions?

FSA contributions are typically confirmed by a range from your employer and must be used within the plan year, with limited carryover options. Health Savings Account (HSA) contributions can come from both you and your employer, and the funds roll over from year to year, allowing for more flexibility and savings growth.

Can you participate in both an FSA and an HSA simultaneously?

You can participate in both an FSA and an HSA if your FSA is a Limited Purpose FSA. This type of FSA only covers certain expenses, such as dental and vision care. Regular FSAs typically prevent simultaneous HSA participation, so is is not common. This makes it very important to understand the types available to you.

What are the advantages of enrolling in an FSA during the open enrollment period?

Enrolling in an FSA during open enrollment lets you set aside pre-tax dollars for eligible healthcare expenses. This reduces your taxable income, saving you money throughout the year. FSAs also provide a way to budget for predictable out-of-pocket expenses, making healthcare costs more manageable.

You may also like…

- How political elections affect the workplace & work benefits

- Open Enrollment S1: What is an HSA?!?!!?

- Open Enrollment S2: Clearing up the confusion about FSA & HSA

Subscribe to my channel

Subscribe to my channel