Does talking about money or your income feel uncomfortable? Do you get stuck when you’re asked how much money you want to make? Are you trying to figure out why personal finance is important? Do you feel like personal financial management tips can help you stop the hustle of living paycheck to paycheck?

These are the 7 tips to guide you through making all of these questions much easier for you.

Managing your money effectively is a critical life skill that can help you understand the amount of money you need to earn from working, achieve your financial goals, and lead a comfortable life. Whether you want to know how much to negotiate a job offer for, save for a rainy day, pay off debt, or invest for your future, you need to have a good understanding of personal finance and the principles of money management.

This post is all about using seven money tips to guide you through money management.

To start managing your money, you need to understand personal finance and the different aspects of money management. This includes setting financial goals, creating a budget, tracking your spending, saving strategies, investment principles, credit management, tax planning, and more. By learning about these topics, you can develop a solid financial plan that aligns with your goals and helps you make the most of your money.

In this article, we will explore the different aspects of money management and provide you with practical tips and strategies to help you manage your money effectively. From understanding personal finance to understanding your minimum income to setting financial goals, we will cover everything you need to know to take control of your finances and achieve financial success.

1. Understanding Personal Finance

Managing your money can be a daunting task, but understanding personal finance is an essential part of leading a successful life. By mastering the basics of budgeting, emergency funds, and debt management, you can take control of your finances, stand firm during job offer negotiations, and build a secure financial future.

Budgeting Basics

Budgeting is the foundation of personal finance. Most folks say that they do not budget because they do not want to limit their money. If you struggle with managing money, then a budget will literally give you flexibility and comfort in spending money. It involves creating a plan for your income and expenses, so you can track your spending and make sure you’re not overspending. Budgeting will literally change your life – for the better! There are several budgeting methods you can use, such as the envelope system, the 50/30/20 rule, or the zero-based budget.

To create a budget, start by listing all of your income (full-time job, part-time job, and side hustles) and your fixed expenses, such as rent, utilities, and insurance. Then, calculate your variable expenses, such as groceries, entertainment, and clothing. Finally, subtract your expenses from your income to see how much you have left over.

When I initially started budgeting, this was difficult for me. I started with pen and paper to create a spending journal. That did not work well. Many times, I forgot to write down if I bought a cup of coffee or grabbed snacks from the snack machine at work. Then, I decided to stop spending cash and group all of my expenses from my banking statement. This really helped me turn things around. I realized that I spent more money on gas, getting my hair done, and partying than I initially thought or even wrote down in my spending journal. DON’T GIVE UP! It’s hard but it’s extremely worth it. I promise you.

As a single mom with two jobs and side hustles, it started as a stressful task. It was when I started taking my feelings out of it and looked at the expenses as literally numbers instead of money I spent, that I noticed a huge difference.

Emergency Funds

No matter how well you budget, unexpected expenses can still arise. That’s why it’s important to have an emergency fund. An emergency fund is a savings account that you can use to cover unexpected expenses, such as car repairs, medical bills, or job loss.

To build an emergency fund, start by setting a savings goal, such as $1,000. That could be in a savings account that is easily accessible to you where you can either get the money quickly or one where it may take two to three days to get access to that money. It is not a bad idea to have two emergency funds. After saving $1,000 in an account that you can easily get into, then start a second savings account and save three to six months’ worth of living expenses.

Personally, when I put the second savings in a completely different bank with no ATM card, that was when I was able to save far more than I ever had before. To take it up a notch, I save money in a bank that is not open on the weekends either. This means, that if I needed that money, I had more than enough time to determine if it should come from that account or be a delayed decision. If it was a delayed decision, then I created a sinking fund for that cost where I saved money over time.

For both accounts, set up automatic transfers from your checking account to your savings account each month or each payday. Make sure your emergency fund is easily accessible, but not so easily accessible that you’re tempted to dip into it for non-emergencies. Yes, it took me a while to realize that my hair appointments and getting the deposit for a trip were not emergencies. Those are now scheduled according to my paycheck and/or are sinking fund expenses. It is up to you where you want to save the sinking fund money. Personally, I add it to my $1,000 account because I know that anything over $1,000 is what I’ve saved towards that goal.

Do what works for you and it may take trying a few ways before settling on the best way for you.

Debt Management

Debt can be a significant obstacle to achieving your financial goals. According to Google, debt is the amount owed by a borrower to the lender. To manage your debt, start by creating a debt repayment plan. You will create this plan by listing all your debts, including the balance, interest rate, and minimum payment. Then, prioritize your debts and focus on them paying off.

Some people organize their debt by the interest rate so that they pay off the card with the highest interest rate first. This helps them to save money by not paying all of the intended interest. Other people, like myself, organize their debt by the lowest debt first. This helps to get small wins along the way and the feeling of accomplishment instead of defeat.

Consider consolidating your debt with a personal loan or a balance transfer credit card. This can help you save money on interest and simplify your debt repayment plan by paying one payment per month towards all of your debt in one payment. If not, consider getting more income through temporary income such as a part-time job or side hustle. Most importantly, avoid taking on new debt. Do not get any new loans or borrow any money at all. Focus on paying off your existing debt as quickly as possible.

This can be done on a low-income budget. I did it myself and shared how I did this in my video titled “Financial Freedom: Crushing Debt on a Budget”. Click the title or the picture above to see how practical and achievable it is to pay down or pay off debt with a low income.

By understanding the basics of personal finance, you can take control of your finances and build a secure financial future. You will also stand firm against job offers with salaries lower than your budget can support. Later, this will make you focus more on knowing the salary for a position early in the interview process or even prior to applying for that job.

Start by creating a budget, building an emergency fund, and managing your debt. With time and effort, you can achieve your financial goals and live the life you want.

2. Setting Financial Goals

Managing your money effectively requires setting financial goals. When you have a clear idea of what you want to achieve financially, you can create a plan to make it happen. Here are some tips to help you set financial goals that are realistic and achievable.

Short-Term Goals

Short-term goals are those that you can accomplish within a year or less. They are important because they help you build momentum and stay motivated. Some examples of short-term financial goals include:

- Creating a budget: A budget is a plan for how you will spend your money. Creating a budget can help you identify areas where you can cut back on spending and save more money.

- Building an emergency fund: An emergency fund is money that you set aside to cover unexpected expenses. Aim to save enough to cover at least three to six months of living expenses. Emergency funds can include money for sinking funds too. It’s up to you!

- Paying off debt: If you have credit card debt, car loan, or other high-interest debt, paying it off should be a top priority. Make a plan to pay off your debt as quickly as possible.

Long-Term Goals

Long-term goals are those that take more than a year to accomplish. They require patience and persistence but can have a big impact on your financial well-being. Some examples of long-term financial goals include:

- Saving for retirement: Retirement may seem far off, but it’s important to start saving early. Consider opening a retirement account, such as an IRA or 401(k), and contribute regularly.

- Buying a home: If you want to buy a home, start saving for a down payment. Aim to save at least 20% of the purchase price to avoid paying private mortgage insurance (PMI).

- Starting a business: If you have an entrepreneurial spirit or are very passionate about something, starting a business can be a great way to build wealth. Create a business plan and start saving for startup costs or look into grants for your business. There are many businesses that require little to no start-up costs and honestly, Heyyy HR! is an example of a business that took low costs to start.

Remember, setting financial goals is just the first step. To achieve your goals, you need to create a plan, stick to it, and make adjustments as needed. If possible, having an accountability partner would be very helpful. You do not need an accountability partner. I was not good at money and I did not have an accountability partner. It was hard, but it was very possible. By taking control of your finances and setting clear goals, you can build a solid financial foundation for the future and truly live the life you want or a life that is beyond your dreams.

3. Saving Strategies

When it comes to managing your money, saving is one of the most important things you can do. Pay attention. This did not say it was EASY, but it says it is IMPORTANT.

Here are a few strategies to help you save more effectively:

High-Interest Savings Accounts

One of the easiest ways to save money is to open a high-interest savings account. These accounts typically offer higher interest rates than traditional savings accounts, which means you can earn more money on your savings over time. Some popular options include Ally Bank, Discover Bank, and Marcus by Goldman Sachs.

Certificates of Deposit

Certificates of deposit (CDs) are another great way to save money. With a CD, you agree to keep your money in the account for a set period of time, such as six months or a year. In exchange, you’ll earn a higher interest rate than you would with a traditional savings account. Just be aware that if you need to withdraw your money early, you may have to pay a penalty.

Automatic Savings Plans

Finally, consider setting up an automatic savings plan. With this type of plan, you can have a certain amount of money automatically transferred from your checking account to your savings account each month. This makes it easy to save money without having to think about it. Many banks and credit unions offer automatic savings plans, so be sure to check with your financial institution to see what options are available.

Over time, I realized that having money automatically deposited to my savings account directly from my paycheck/employer was the easiest way. I do not like having others in my personal business and in most cases, I either had to make this request through the Human Resources Department or the Finance Department. This forced me to set up the auto-deposit and leave it there.

By utilizing these saving strategies, you can build up your savings over time and achieve your financial goals. You may surprise yourself and achieve these goals faster than you ever imagined.

4. Investment Principles

When it comes to managing your money, investing can be a powerful tool to help grow your wealth over time. Miriam Webster defines wealth as an abundance of valuable material possessions or resources. However, it’s important to understand the principles of investing before diving in.

Here are a few investment principles to keep in mind:

Stock Market Fundamentals

Investing in the stock market can be a great way to grow your wealth over time, but it’s important to understand the fundamentals of the stock market before investing. The stock market is a complex system, and it’s important to have a basic understanding of how it works before investing.

Some key concepts to understand include:

- Stock prices are determined by supply and demand

- The stock market is influenced by a variety of factors, including economic indicators, geopolitical events, and company-specific news

- Investing in individual stocks can be risky, so diversification is important

Before starting to invest in the stock market, I highly suggest contacting a financial professional to help you decide where to start and to have them monitor activity over time. Nick Grant and his team at Premier Financial Group have been a huge help to me in all types of investing, as well as retirement preparation.

Retirement Accounts

Retirement accounts can be a great way to save for retirement and grow your wealth over time. It is important to prepare for retirement as if you will not get Social Security Benefits. Typically, Social Security Benefits do not offer enough monthly income to take care of your living expenses in a comfortable way. In addition, retirement accounts help you to not live on what most call “a fixed income” or at least to not live on such a strict or limited fixed income.

There are several different types of retirement accounts to choose from, including:

- 401(k)s: These are employer-sponsored retirement accounts that allow you to contribute pre-tax dollars to your retirement savings. Many employers also offer matching contributions, which can help boost your savings.

- Individual Retirement Accounts (IRAs): These are individual retirement accounts that allow you to save for retirement on your own. There are two main types of IRAs: traditional and Roth. Traditional IRAs allow you to contribute pre-tax dollars, while Roth IRAs allow you to contribute after-tax dollars.

- Social Security: Social Security is a government-run retirement program that provides retirement benefits to eligible individuals. The amount of your Social Security benefit is based on your earnings history and the age at which you begin receiving benefits.

Diversification Strategies

Diversification is an important principle of investing. By diversifying your investments, you can help reduce your overall risk and potentially increase your returns. Some diversification strategies to consider include:

- Investing in a mix of stocks, bonds, and other asset classes

- Investing in both domestic and international markets

- Investing in both large and small companies

Overall, investing can be a powerful tool to help grow your wealth over time. These types of diversifying strategies are not a “get rich over night” type of investment. Over time, you get a large return on your investment while saving large sums of money. By understanding the principles of investing and developing a solid investment strategy, you can help achieve your financial goals.

5. Expense Tracking and Reduction

Managing your money involves more than just earning money or increasing your income and saving. It also requires keeping track of your expenses and finding ways to reduce them. Here are some tips on how to track your expenses and cut down on unnecessary spending.

Tracking Tools

One of the most important steps in managing your expenses is to track them. There are many tools available to help you do this, from budgeting apps to spreadsheets. Bank of America had some great online options that I took advantage of, those options were very helpful and I was able to achieve a lot of my financial goals with their guidance.

Some other popular options include:

- Mint: A free budgeting app that allows you to link your bank accounts and credit cards to track your spending and create a budget.

- Personal Capital: A free financial management tool that allows you to track your net worth, investments, and expenses.

- Excel: A spreadsheet program that allows you to create your own budgeting templates and track your expenses manually. If you have a Gmail account, then using Google Sheets is free and far more convenient than Microsoft Excel.

Cutting Unnecessary Spending

Once you have a good idea of where your money is going, it’s time to start cutting back on unnecessary expenses. Cutting back on unnecessary spending instantly impacted my financial standing. The first thing I noticed was that I started having money left over or “extra money” after I paid all of my bills each pay period.

Here are a few areas where you can potentially save money:

- Eating out: One of the biggest expenses for many people is eating out. Consider cooking at home more often or packing your lunch for work. Meal planning is helpful too because it forces you to prepare ahead of time and commit to a schedule. Over time this breaks bad habits.

- Entertainment: Cut back on subscriptions to services you don’t use often, like cable TV or streaming services. Initially, cutting cable is difficult but after roughly 3 months, you won’t realize that you no longer have it. Though I wasn’t able to do this all at once, eventually, I replaced all of my TVs to wifi acceptable TVs, and then changed to limited streaming services.

- Shopping: Avoid impulse purchases and wait for sales or discounts before making a purchase. Eventually, learn sales schedules for your favorite store, the best seasons of the year to purchase certain items and you’ll save a lot of money while still getting what you want or need.

Negotiating Bills

Another way to save money is to negotiate your bills. Many service providers, like cable companies or cell phone providers, offer discounts to customers who ask for them. Use your length of time having their service in your favor, as well as, your successful payment history. Even if you are only able to get a temporary discount, you were able to save some money or use it for another purpose.

Here are a few tips for negotiating your bills:

- Research: Do your research and find out what other providers are offering for similar services. Ask in Facebook groups because others will share.

- Be polite: Approach the conversation with a friendly and polite tone.

- Be persistent: If the representative you’re speaking with can’t help you, ask to speak with a supervisor or hang up and call right back to get another rep.

By tracking your expenses, cutting unnecessary spending, and negotiating your bills, you can take control of your finances and work towards your financial goals.

6. Credit Management

Managing your credit is important for your financial health. It can affect your ability to get loans, credit cards, and even rent an apartment. Many credit cards or loans will offer money or incentives to you that can save you money in other areas when you have good credit. Airline credit cards or cards like Capitol One and Chase will give you incentives like free checked bags or buddy passes.

Here are some tips to help you manage your credit.

Understanding Credit Scores

Your credit score is a three-digit number that represents your creditworthiness. It is based on your credit history, including your payment history, credit utilization, length of credit history, and types of credit used. The higher your credit score, the better your creditworthiness. The score ranges from 300 to 850. The higher your credit score the better your creditworthiness.

You can check your credit score for free once a year from each of the three major credit bureaus: Equifax, Experian, and TransUnion. The best place to get your credit report annually with no impact on your credit score is annualcreditreport.com.

You can also use free credit monitoring services to keep an eye on your credit score and report. Now, many credit cards will show at least one of your credit scores on your monthly statement. You can also use apps like Credit Karma, Experian, and Credit Sesame to monitor 1-2 of your credit scores and changes to your credit report at little to no cost.

Building Good Credit

To build good credit, you need to use credit responsibly. This means paying your bills on time, keeping your credit card balances low, and only applying for credit when you need it. Maintaining a credit balance that has only used 10-30% of your available credit will definitely keep you in good credit standing and increase your credit score and/or credit limit over time.

One way to build credit is to get a secured credit card. This type of credit card requires a deposit, which serves as collateral. You can use the card like a regular credit card, but your credit limit is equal to the amount of your deposit. Most people who opt for a secured credit card use this option when they are not able to get approved for a non-secured credit card.

Another way to build credit is to become an authorized user on someone else’s credit card. This allows you to use their credit card, but the primary cardholder is responsible for the payments. This is an immediate impact on your credit score. As long as they maintain on-time payments, keep the credit balance low, and keep that line of credit open, your credit score will increase and so will their credit score.

Credit Report Monitoring

It’s important to monitor your credit report regularly to ensure that there are no errors or fraudulent activity. Review your free copy of your credit report once a year from each of the three major credit bureaus.

If you notice any errors or fraudulent activity, you should dispute it with the credit bureau and the creditor. You can also consider using a credit monitoring service or a credit monitoring app that alerts you to any changes in your credit report.

By understanding credit scores, building good credit, and monitoring your credit report, you can manage your credit effectively and improve your financial health.

How I Went From a 545 Credit Score to an AMAZING 707

7. Tax Planning

Managing your finances involves more than just earning and spending money. You also need to ensure that you’re paying the correct amount of taxes. Tax planning is the process of analyzing your financial situation to maximize your tax deductions and credits and minimize your tax liability.

Here are some key aspects of tax planning that you should be aware of:

Tax Deductions

Tax deductions are expenses that reduce your taxable income. Some common tax deductions include mortgage interest, charitable donations, and medical expenses. By taking advantage of these deductions, you can reduce your taxable income and lower your overall tax bill. It’s important to keep track of your expenses throughout the year and make sure you have the necessary documentation (i.e. payment receipts) to support your deductions.

Tax Credits

Tax credits are even more valuable than deductions because they directly reduce your tax liability. Some common tax credits include the earned income tax credit, the child tax credit, and the American Opportunity Tax Credit (AOTC). To claim these credits, you’ll need to meet certain eligibility requirements and provide the necessary documentation. Make sure you’re taking advantage of all the tax credits you’re eligible for to maximize your tax savings. Tax professionals are a great resource to guide you with tax credits and how to earn them in the future.

Tax-Advantaged Investments

Tax-advantaged investments are investments that offer special tax benefits. Some examples include 401(k) plans, individual retirement accounts (IRAs), and health savings accounts (HSAs). By investing in these accounts, you can reduce your taxable income and defer taxes on your investment earnings. It’s important to understand the rules and restrictions associated with each type of account to make the most of your tax-advantaged investments.

Overall, tax planning is an important part of managing your finances. By understanding the various tax deductions, credits, and investment options available to you, you can minimize your tax liability and keep more of your hard-earned money.

Key Takeaways

- Understanding personal finance is essential for effective money management.

- Setting financial goals and creating a budget can help you stay on track and achieve your objectives.

- Saving strategies, investment principles, credit management, and tax planning are all critical components of managing your money effectively.

Frequently Asked Questions (FAQs)

What are the best strategies for budgeting as a beginner?

If you are new to budgeting, it can be overwhelming to know where to start. One of the best strategies for budgeting as a beginner is to track your spending. This will help you understand where your money is going and where you can cut back. You can use a spreadsheet, your banking statement, online banking access, or a budgeting app to track your expenses and income. Another strategy is to create a realistic budget and stick to it. This means setting aside money for your bills, savings, and discretionary spending. Automating your savings and bill payments to make it easier to stay on track.

How can students effectively manage their finances?

Managing finances as a student can be challenging, but there are several strategies that can help. First, create a budget and stick to it. This means setting aside money for your tuition, books, rent, food, and other expenses. If those other expenses include going out with friends to dinner or out to a party, then add the amount you intend to spend to your budget. This will keep you from having financial surprises and freedom with your money. You should also look for ways to save money, such as buying used textbooks or cooking meals at home instead of eating out. Another strategy is to take advantage of student discounts and scholarships. You should also consider working part-time to earn extra money and gain valuable experience.

What are some tips for managing finances together as a couple?

Managing finances as a couple can be challenging, but there are several tips that can help. First, be open and honest about your finances. This means discussing your income, expenses, debts, and financial goals. You should also create a joint budget and stick to it. This means setting aside money for your bills, savings, and discretionary spending. You should also consider opening a joint bank account and automating your bill payments and savings. Another tip is to communicate regularly about your finances and make adjustments as needed.

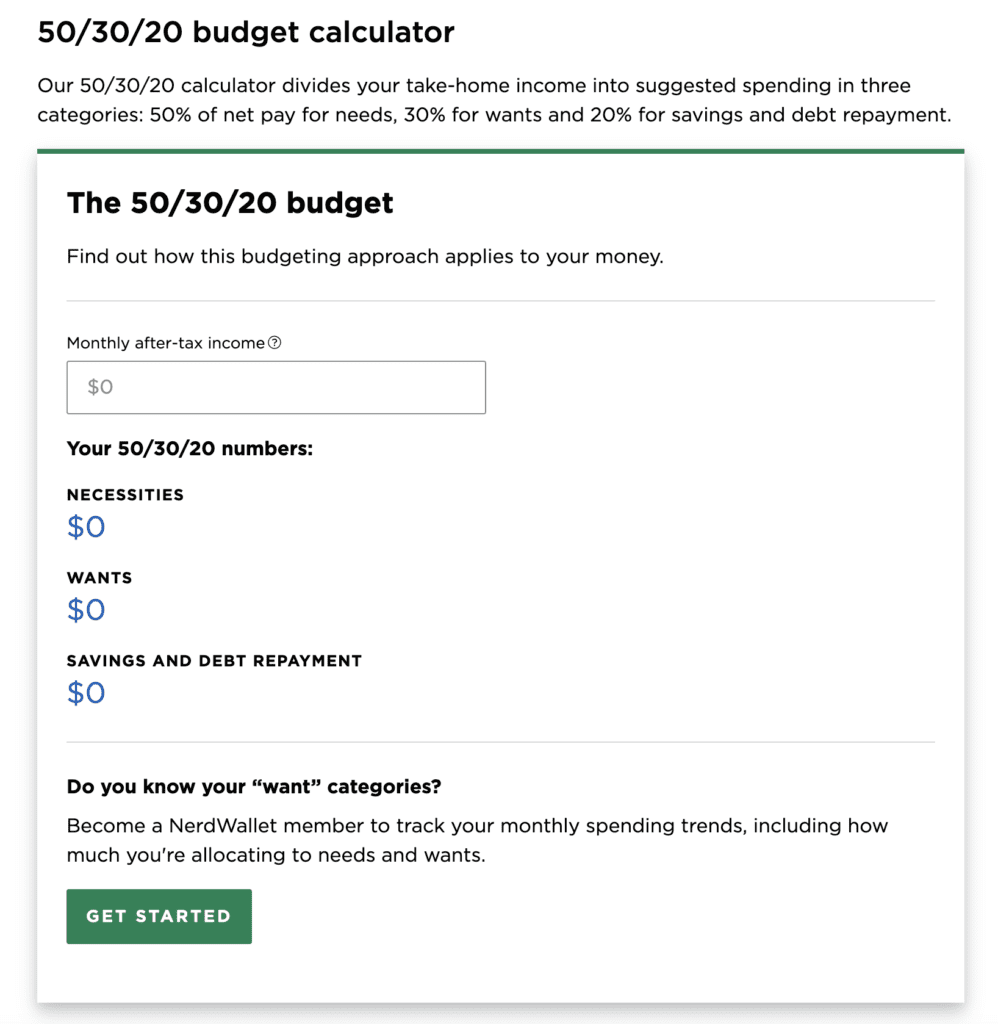

What is the 50/30/20 budgeting rule and how can it be applied?

The 50/30/20 budgeting rule is a popular budgeting method that can help you manage your finances. The rule suggests that you allocate 50% of your income to your needs, 30% to your wants, and 20% to your savings and debt repayment. This means setting aside 50% of your income for essentials like rent, utilities, and groceries, 30% for discretionary spending like entertainment and dining out, and 20% for savings and debt repayment. You can apply this rule by creating a budget and allocating your income accordingly.

How should one approach financial planning in their 20s?

Financial planning in your 20s is important because it sets the foundation for your future financial success. One approach is to create a budget and stick to it. This means setting aside money for your bills, savings, and discretionary spending (including fun activities like movies, dinner, partying, etc). You should also focus on paying off high-interest debt and building an emergency fund. Honestly, it would be best to avoid debt if at all possible during your 20s or until you get comfortable living according to your budget. Another strategy is to start investing early and regularly. This means taking advantage of your employer’s retirement plan and opening a brokerage account to invest in stocks and bonds.

What are the key components of a solid financial management plan?

A solid financial management plan should include several key components. First, it should include a budget that outlines your income, expenses, and savings goals. This means setting aside money for your bills, savings, and discretionary spending (i.e. eating out, vacations, clothing, etc.). Second, it should include a debt repayment plan that focuses on paying off high-interest debt. Third, it should include an emergency fund that can cover unexpected expenses. Fourth, it should include a retirement plan that helps you save for your future. Finally, it should include a strategy for investing that aligns with your goals and risk tolerance.

You may also like…

- Discover How HR Pros Can Make Money on the SIDE!

- Financial Freedom: Crushing Debt on a Budget

- Finances 101: Essentials for Personal Money Management

- How I Went From a 545 Credit Score to an AMAZING 707

Subscribe to my channel

Subscribe to my channel