Student loan debt can quickly become overwhelming, especially if you fall behind on payments. If your federal student loans go into default, the government can begin collecting money from you, often through methods like wage garnishment or seizing tax refunds. More than 5 million borrowers are now at risk of facing these mandatory debt collections, which have recently resumed after a pause during the pandemic.

Most student loan borrowers were under the assumption that they had far more time to begin repayment since President Biden’s student loan repayment pause. Now, the Trump Administration has stated that it will resume federal student loan debt collection for any borrowers who are behind in payments. This is expected to start on May 5, 2025.

Understanding how student loan debt collection works is the first step to protecting your finances. Collection actions are serious and can have long-lasting effects on your credit and paycheck if not handled quickly. Knowing what steps you can take if your loans are in default gives you a better chance to regain control. Those who are in default or behind on their payments will be given a 30-day notice before wage garnishments, tax refunds are seized, and other financial reprimands are put in place.

Understanding Student Loans and Debt Collection

When you fall behind on your student loans, several steps can be taken. Your lender has legal ways to collect the money you owe, and the process can affect your everyday purchases, long-term finances, ability to buy a house or car, and so many other aspects of your daily life.

How Student Loan Debt Collection Works

If you do not pay your federal student loans, your loan may be placed into default. This usually happens when you have not made a payment for 270 days. After default, the full balance becomes due at once.

Debt collection may start with written notices, phone calls, and possibly emails. If you still do not pay, collection agencies can get involved. For federal loans, the government may collect your debt by taking your tax refund, reducing your Social Security payments, or garnishing your wages.

You may also be charged collection fees, increasing the total debt. Private student loan collections are different, and lenders often need court approval before they can take money from your paycheck or bank account.

Key facts:

- Wage garnishment is common with federal student loans in collections

- Your credit score can be lowered

- Extra fees may be added to what you owe

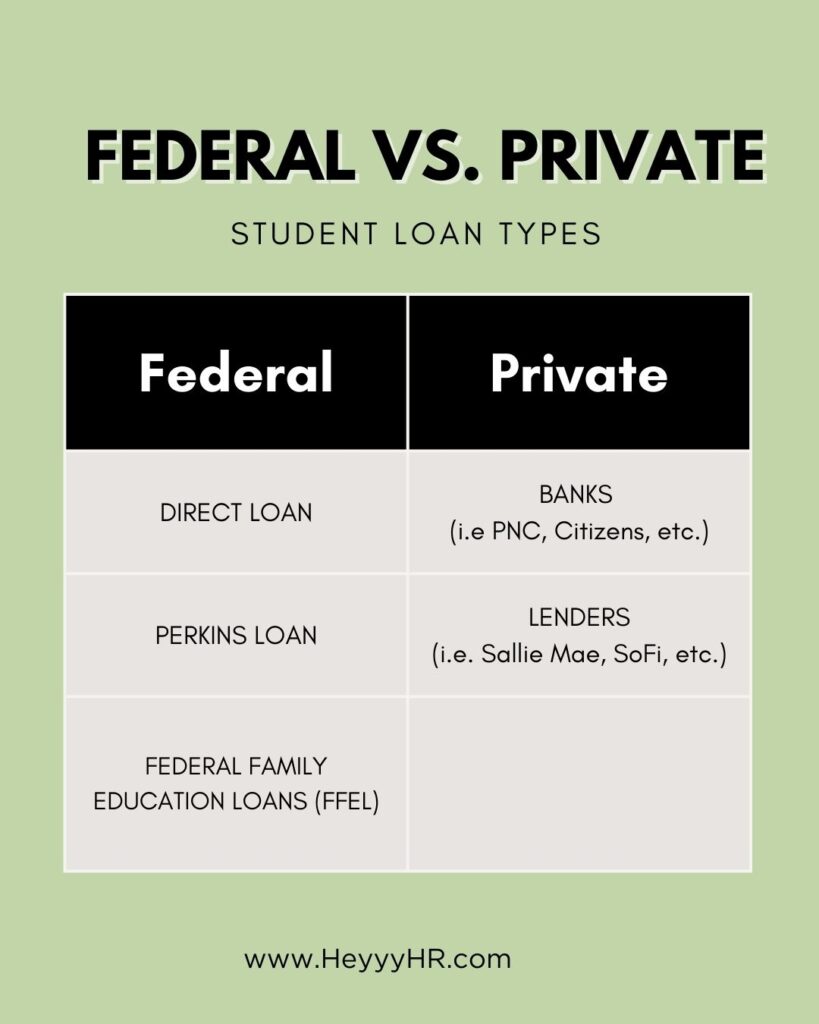

Types of Student Loans in Collections

There are two main types of student loans that can end up in collections: federal loans and private loans.

Federal student loans include Direct Loans, Federal Family Education Loans (FFEL), and Perkins Loans. The government has many ways to collect unpaid federal loans that private lenders do not. For example, federal loans can be collected through tax refund withholding or wage garnishment without going to court.

Private student loans are offered by banks and other private lenders. If you default, private lenders usually need a court order before they can garnish wages or take other actions.

| Loan Type | Collection Agency | Wage Garnishment | Tax Refund Offset | Court Order Needed |

|---|---|---|---|---|

| Federal | Yes | Yes | Yes | No |

| Private | Yes | Sometimes | No | Yes |

Common Reasons for Student Loan Default

You may default on your student loan for many reasons. Some of the main causes include:

- Job loss or a drop in your income

- Not understanding the repayment terms

- Forgetting to update contact information, so you miss important notices

- Paying other bills first because of limited funds

Health problems, divorce, additions to the family (or childbirth), mental health issues, or family emergencies can make it even harder to keep up with payments.

Default can happen even if you miss payments by accident. Ignoring bills or not contacting your loan servicer often makes the situation worse. Many people do not know about options like deferment, forbearance, or income-driven repayment plans, which may help avoid default.

Managing Student Loan Debt Collection

If you fall behind on your student loan payments, collection efforts can start quickly. The Trump Administration has planned to start collection efforts no later than 30 days after notifying borrowers of their payment requirements. Understanding your rights, ways to work with collectors, and the consequences of ignoring debt collection are essential for protecting your finances.

Rights and Protections for Student Loan Borrowers

You have specific rights when dealing with student loan debt collectors. For federal loans, collectors must follow rules set by the Fair Debt Collection Practices Act (FDCPA), which limits when and how they can contact you. They cannot harass or threaten you, and you can request written proof of your debt.

If your federal loans are in default, your loan holder may garnish up to 15% of your disposable wages or take your tax refunds without suing you in court. However, you have the right to ask for a hearing to challenge the garnishment or to set up a payment plan.

With private loans, collectors often need a court order before they can garnish your wages or take further legal steps. Always keep records of any communication and payments you make during this process.

Negotiating Repayment Terms

You can work with the collection agency to set up new payment terms. For federal loans, you might be able to rehabilitate the loan by making a set number of agreed-upon payments, or consolidate the debt into a new loan with a more manageable monthly payment. This can remove the default from your credit report and end wage garnishment.

Private loan collectors may allow you to negotiate a lump-sum settlement or a payment arrangement that lowers your monthly cost. Always get any new agreement in writing.

For both types, be clear about your financial situation and only agree to payments you know you can handle/afford each month. If you are unsure about your rights or need help, consider speaking to a credit counselor or a legal aid organization.

Consequences of Ignoring Collection Efforts

Ignoring collection efforts has serious effects. The government can resume collections on defaulted student loans, garnish your wages, and withhold federal or state tax refunds automatically.

Your credit score will drop, making it harder to borrow money, finance a car, or rent an apartment. For private loans, if the collector goes to court and wins a judgment, they can use legal tools like wage garnishment or bank account levies.

Unpaid balances may keep growing because of collection fees and interest. Staying in contact with the collector and responding to notices is the best way to avoid extra costs and long-term financial problems.

Avoid Student Loans Being Reported to Collections

Here are three steps someone should take immediately to avoid their student loans being reported to collections under the Trump administration’s 2025 stance:

1. Contact Your Loan Servicer Immediately

If you’ve missed payments or are unsure of your status, call or log in to your loan servicer’s portal right away.

Ask:

- Am I in default?

- Is my loan delinquent?

- What are my repayment options?

If you’re more than 90 days late, your loan can be reported to credit bureaus. After 270 days (for federal loans), it can go to collections.

2. Apply for an Income-Driven Repayment Plan (IDR)

2. Apply for an Income-Driven Repayment Plan (IDR)

If you’re struggling to afford payments, apply for an Income Driven Repayment (IDR) plan request.

These plans:

- Lower monthly payments based on your income and family size

- Can be as low as $0/month if your income is low enough

- Keep your loan in good standing (even with low or no payments)

You can apply for an IDR online via studentaid.gov and often get an immediate estimate.

3. Request a Forbearance or Deferment (if you qualify)

If you recently lost your job, had a medical issue, or are in school, you may qualify to temporarily pause payments.

- Forbearance: Temporary stop due to financial hardship or illness

- Deferment: Usually available for school, unemployment, or military service

Just remember that even with these options, interest often continues to accrue, but it’s better than falling into default.

Key Takeaways

- Student loan default can lead to wage garnishment and other collection actions.

- Staying informed helps you manage and avoid debt collection issues.

- Knowing your options can make it easier to handle student loan problems.

Frequently Asked Questions (FAQs)

Student loan debt can impact your credit, financial stability, and future finance-related options. Knowing your rights and understanding how collections work can help you make informed choices.

What are the consequences of student loans defaulting and being sent to collections?

If your student loan goes into default, your entire balance may become due right away. Debt collectors may contact you frequently. Your credit score also drops, and you may face wage garnishment or loss of tax refunds. For federal loans, the government can collect directly, including taking your tax return or part of your paycheck. Learn more about collections after default from Federal Student Aid’s Collections on Defaulted Loans.

How can one challenge the legitimacy of student loan debt claimed by collection agencies?

You have the right to ask for proof that you owe the debt. Ask the collection agency for a written “validation notice” that details what you owe and to whom. If you believe the debt is not yours or the amount is wrong, send a written dispute to the collector. The agency must stop collecting until they verify the debt. Read about your rights under the Fair Debt Collection Practices Act at the FTC’s Debt Collection FAQs.

What services are available to assist individuals struggling with student loan debt?

Federal loan servicers offer options like income-driven repayment plans, deferment, and forbearance. Non-profit credit counseling agencies can also help you make a plan and understand your choices. If you suspect fraud or need help dealing with a third-party company, federal servicers often have resolution units you can contact. Edfinancial explains what documents to send and where at their Frequently Asked Questions.

Are there reputable websites that specialize in student loan debt advice and management?

Yes, a few government-backed and non-profit sites offer trustworthy advice and resources. The official Federal Student Aid website gives information about managing loans and what to do if you’re behind on payments. The Federal Student Aid collections page is a good place to start for those in or near default.

What does it mean when a student loan is categorized as defaulted, and what implications does this have?

A loan is called “defaulted” when you haven’t made payments for a set amount of time, usually 270 days for federal loans. Defaulting leads to the loan being reported to credit bureaus, lowering your credit score, and possibly being sent to a collection agency.

How do forbearance and collections interact in the context of defaulted student loans?

Forbearance is an option to temporarily pause payments or lower your payment amount, but it is not usually offered if your loan is already in collections. Once in collections, you must often resolve your default or make arrangements to get out of default before forbearance can be considered again. For more on loan servicing rules, see the Department of Education’s Loan Servicing and Collection Frequently Asked Questions.

You May Also Like …

- Federal Student Aid: Collections and Defaulted Loans

- Fair Debt Collection Practices Act (FDCPA)Discover

- How You Can Make Money using SIDE-HUSTLES!

- Credit Score Optimization: Strategies for Financial Health

Subscribe to my channel

Subscribe to my channel